Stop Chasing Stock Prices: The Real Secret to Wealth Creation

Master the art of valuation to stop gambling and start investing.

INVESTING

3/26/20264 min read

The Invisible Scorecard: Why Everything You Know About Business Success is Wrong

Every company on this planet tells a story. Some speak of explosive growth, others of revolutionary innovation, and some simply of survival. But behind the glossy annual reports and the frantic ticking of stock tickers, there is a deeper, more haunting question that most people—even seasoned professionals—fail to answer correctly: Is this company actually creating value?

We live in an era of activity. We celebrate a startup for hiring a thousand people in a month. We cheer when a corporation expands into a new continent. We check our brokerage apps and feel a surge of dopamine when a green line moves upward. But here is the cold, hard truth: activity is not progress, and stock price movement is not performance.

I have spent years dissecting businesses, and if there is one thing I’ve learned, it’s that hope is not a strategy. Only disciplined thinking turns effort into value. If you want to stop gambling with your capital—whether you are an investor, a founder, or a manager—you must learn the language of the invisible scorecard.

1. The Core Identity: Is the Engine Efficient?

Before you look at how fast a company is growing, you must look at how hard its money is working. Most investors obsess over net income, but profit is an opinion shaped by accounting rules. Cash flow is the reality. To see the truth, we use Return on Invested Capital (ROIC).

NOPLAT: Net Operating Profit Less Adjusted Taxes (The actual cash profit from the engine).

Invested Capital: The total money tied up in the machine (Factories, software, inventory).

The Reality Check: Beta Tech vs. Legacy Corp

Imagine Beta Tech generates $90M in NOPLAT using $500M of capital. Its ROIC is 18%.

Now imagine Legacy Corp also generates $90M, but it requires $1,000M in old factories and heavy inventory to do it. Its ROIC is only 9%. Even though their profits look identical on a news crawler, Beta Tech is a vastly superior machine. It creates twice as much value with the same dollar.

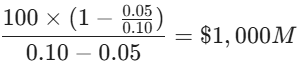

2. The Growth Trap: When Expansion Destroys Wealth

We are conditioned to believe that growth is always good. This is a dangerous lie. Growth only creates value if your ROIC is higher than your cost of capital. If not, growth is a cancer that consumes resources faster than it produces them.

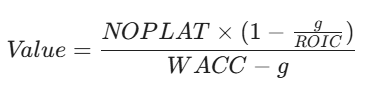

This relationship is captured by the Value Driver Formula, the holy grail of valuation:

Why the Experts Get It Wrong

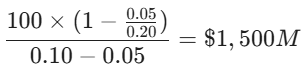

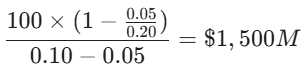

Let’s look at Alpha Corp. They earn $100M and want to grow at 5%. Their cost of money (WACC) is 10%.

Scenario A (High Efficiency): If their ROIC is 20%, the value of the business is:

Scenario B (Low Efficiency): If their ROIC is only 10% (exactly their cost of capital), the value is:

In Scenario B, the growth added zero value to the shareholders. The company spent every penny of that growth just to stand still. When you see a high-growth company with low returns, you aren't looking at a rocket ship; you're looking at a bonfire.

3. The Price of the Dream: What Does Money Cost?

You cannot value a business without knowing the hurdle rate. This is the Weighted Average Cost of Capital (WACC). It represents the blended cost of what you owe the bank (Debt) and what the shareholders expect (Equity).

Re: Cost of Equity (The risk premium shareholders demand).

Rd: Cost of Debt (The interest rate).

t: Corporate tax rate (The tax shield).

A Sample Calculation: Gamma Logistics

Gamma Logistics is funded by 60% Equity (investors want 12% returns) and 40% Debt (at 5% interest). With a 20% tax rate:

If Gamma isn't earning at least 8.8% on its projects, it is failing. It is a borrower that cannot pay back its true economic cost.

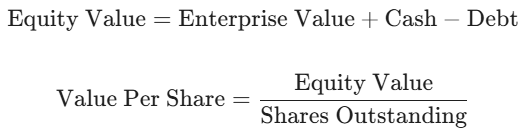

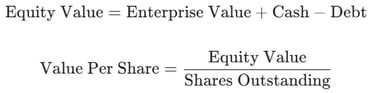

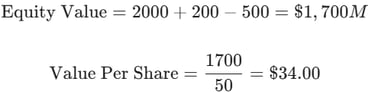

4. The Final Verdict: What Is Your Seat Worth?

Once we know the value of the entire machine (Enterprise Value), we have to pay off the bank to see what is left for us—the owners. This gives us the Intrinsic Value Per Share.

The Moment of Truth

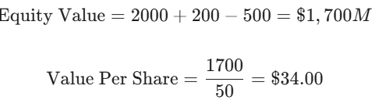

Assume your DCF model says a company’s Enterprise Value is $2,000M. It has $200M in cash but owes $500M in debt. There are 50M shares.

If that stock is trading at $28.00, the market is being pessimistic. If it’s trading at $45.00, the market is high on a narrative that the math doesn't support.

The Architect’s Mindset

Valuation isn't about being a math genius; it's about being a disciplined architect. By using these formulas, you stop being a passenger in the market and start being the one who decides what a seat is worth.

The market is a weighing machine, not a beauty contest. Over the long run, it doesn't care about your disruptive story or your visionary CEO. It only cares about sustainable cash flow and returns on capital.

Stop chasing stock prices. Start measuring the machine. Because in the end, the math always wins.